|

Photo: FAO/FIS

Globefish: 'Pollock prices to continue to decline due to increased catch', Less cod, more pollock

WORLDWIDE WORLDWIDE

Tuesday, July 23, 2024, 01:00 (GMT + 9)

The outlook for 2024 indicates a considerable reduction in the availability of cod; and conversely, that more Alaska pollock will be landed. Thus, price developments for these species will take opposite directions: cod prices will rise while Alaska pollock prices will decline. Surimi production may increase, and prices are expected to slide.

Supplies

The Arctic region, and the Barents Sea in particular, is an area that has enormous resources of groundfish but it is also of importance for other reasons, such as mineral resources. Activities in the Arctic are governed by the UN Convention on the Law of the Sea (UNCLOS), which came into being in the 1970s, and which was signed by the most important Arctic nations, including the Russian Federation. However, the Russian Federation is now reported to be contemplating withdrawing from UNCLOS, because “it is detrimental to Russian interests” and “Russia must prioritize its interests in the Arctic, particularly its vast territorial claims.” Currently, the region’s resources are well-managed by a joint Russia-Norway committee; therefore, any Russian withdrawal from UNCLOS may jeopardize this cooperation and potentially be extremely detrimental to the fisheries resources in the region. The Arctic region, and the Barents Sea in particular, is an area that has enormous resources of groundfish but it is also of importance for other reasons, such as mineral resources. Activities in the Arctic are governed by the UN Convention on the Law of the Sea (UNCLOS), which came into being in the 1970s, and which was signed by the most important Arctic nations, including the Russian Federation. However, the Russian Federation is now reported to be contemplating withdrawing from UNCLOS, because “it is detrimental to Russian interests” and “Russia must prioritize its interests in the Arctic, particularly its vast territorial claims.” Currently, the region’s resources are well-managed by a joint Russia-Norway committee; therefore, any Russian withdrawal from UNCLOS may jeopardize this cooperation and potentially be extremely detrimental to the fisheries resources in the region.

Meanwhile, global warming is affecting Arctic regions particularly strongly; according to researchers at the Norwegian Meteorological Institute, air and water temperatures in the Barents Sea are rising five to seven times faster than the global average. This is forcing the fish stocks to migrate farther north and east, where temperatures are still a bit colder. Meanwhile, global warming is affecting Arctic regions particularly strongly; according to researchers at the Norwegian Meteorological Institute, air and water temperatures in the Barents Sea are rising five to seven times faster than the global average. This is forcing the fish stocks to migrate farther north and east, where temperatures are still a bit colder.

With regard to cod resources, data presented at the 2023 Groundfish Forum last autumn showed that landings of the species have continued to decline over the past eight years, and will continue to do so. A forecast was also presented earlier that showed 2024 landings would fall from 1.3 million tonnes in 2023 to 1.1 million tonnes in 2024.

While cod quotas are down for 2024, Russian scientists are recommending a 12 percent increase in the total allowable catch (TAC) for Alaska pollock in the Far East. At the same time, the Pacific Fisheries Research Centre (TINRO) is proposing a TAC of 2.55 million tonnes for 2024, up 260 000 tonnes compared to the 2023 TAC. The Russian fleet usually does not take up the whole quota, however. In 2023, only 78 percent of the quota was landed, and before that, in 2022 and 2021, the volume landed represented 91 percent and 89 percent of the yearly quotas, respectively. The TAC for Alaska pollock in the West Bering Sea in 2024 is 700 000 tonnes, while the TAC in the Northern Sea of Okhotsk is 342 500 tonnes.

Photo: Rosrybolovstvo

According to the Russian Federal Fishery Agency (Rosrybolovstvo), from January to mid-March 2024, landings of Alaska pollock in the Russian Far East were up by about nine percent, amounting to 750 000 tonnes. The harvest for the whole year (2024) is projected to increase by 12 percent compared to 2023, and will reach 3.7 million tonnes, according to estimates presented at the Groundfish Forum last autumn. This is the highest level in 10 years. These increased landings have pushed domestic prices down by some 23 percent.

Market

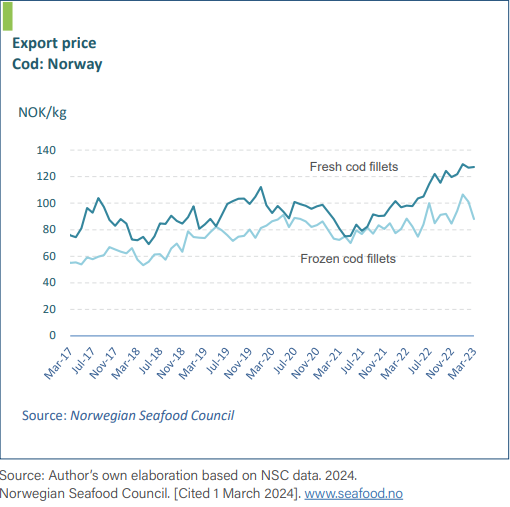

The low landings of cod are creating problems for the processing industry in Europe, and things will get worse in 2024. The tight supplies have pushed prices up tremendously, and prices for Norwegian round-frozen cod are presently about USD 6,000 per tonne. This is some USD 2,000 higher than for Russian cod destined for processing.

At the North Atlantic Seafood Forum (NASF), which was held in Bergen, Norway, in the beginning of March 2024, there was some focus on the development of whitefish prices, especially for cod. It was pointed out that the Barents Sea cod quota for 2024 is down by 20 percent compared to 2023, and expected to drop further in 2025, resulting in less cod on the market.

Experts at NASF expressed expectations of cod prices peaking in 2025, and then perhaps weakening slightly in 2026, when the resource situation is expected to become somewhat better.

This may also mean that less cod will be sold in Europe, for the European economies are currently not in great shape. In fact, European GDP growth is not expected to recover until 2025. The alternative for European consumers could then be cheaper whitefish, like Alaska pollock or farmed tilapia and pangasius. As mentioned above, Alaska pollock supplies will be abundant, and prices tend to be well below cod prices.

Trade

The US ban on imports of Russian fish, which came into effect on 24 February 2022, will probably lead to a 90,000-tonne shortfall of cod (live weight equivalents) on the US market. The import ban now also includes products of Russian origin but processed in a third country. It should be noted that the United Statesimports large quantities of cod fillets from countries like China, Viet Nam and Indonesia, and much of this is based on Russian raw material. These products are now banned.

Norwegian exports of whole frozen cod declined by 23.5 percent in 2023 compared to 2022, amounting to 51 054 tonnes. The strongest decline was registered for China, which took almost 54 percent less cod from Norway; Norwegian exports to China dropped from 66 745 tonnes in 2022 to 51,054 tonnes in 2023. In contrast, exports to other main markets were up from 9,122 tonnes in 2022 to 10,099 tonnes in 2023 for the United Kingdom of Great Britain and Northern Ireland, and from 4,905 tonnes in 2022 to 6,066 tonnes in 2023 for Poland.

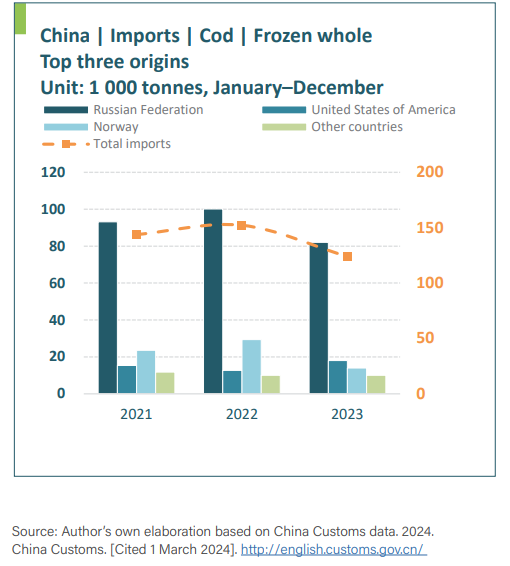

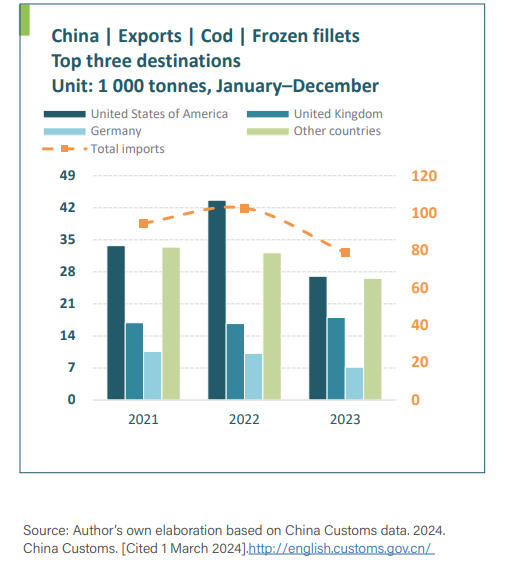

Specific to China, total imports of whole frozen cod were 123,964 tonnes in 2023, a decline of 18.6 percent compared to the previous year. In addition to a considerably reduced volume from Norway as mentioned above, imports from the Russian Federation fell by 18.1 percent to 82 011 tonnes, and from the United States by 42.9 percent to 18,060 tonnes. As expected, Chinese exports of frozen cod fillets also fell; in 2023, exports of the product amounted to 78,804 tonnes, 23.3 percent less than in 2022. The largest drop was registered for exports to the United States , which fell by 38 percent to 27,022 tonnes.

Chinese imports of whole frozen Alaska pollock were 615,706 tonnes in 2023, about the same level as in 2022. About 93.3 percent of this (574,618 tonnes) came from the Russian Federation, much of which was processed into fillets for re-export.

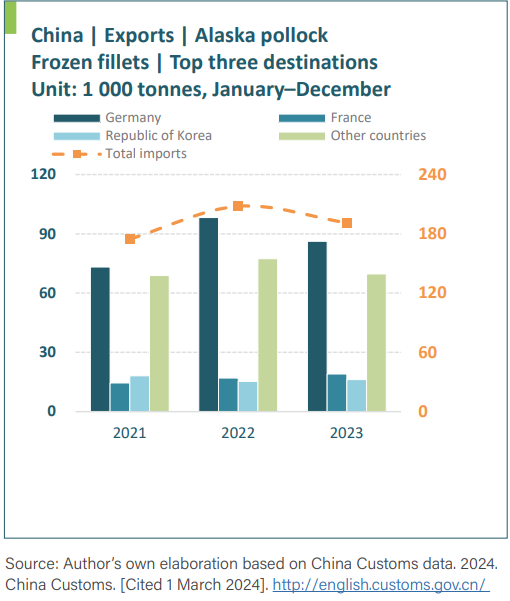

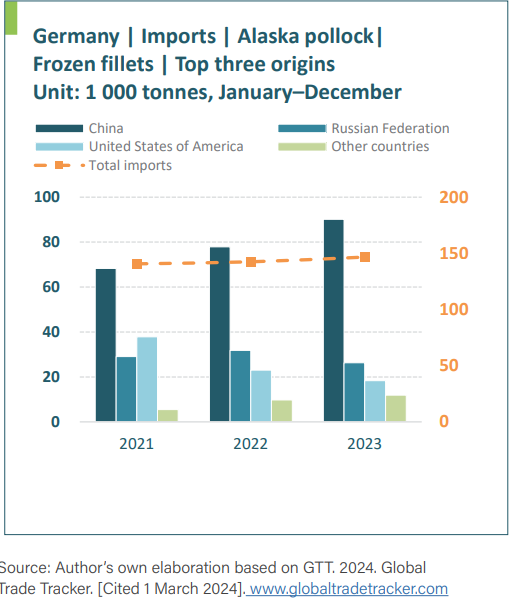

In December 2023, the EU-27 countries imported record volumes of Alaska pollock fillets, mainly from China and the Russian Federation. Nevertheless, Chinese exports of frozen Alaska pollock fillets recorded a drop of 20 percent in that year to 191,175 tonnes. There were some shifts among the markets, too. Exports to Germany fell by 12.2 percent, while exports to France increased by 12.5 percent. Still, Germany accounted for as much as 45 percent of the total.

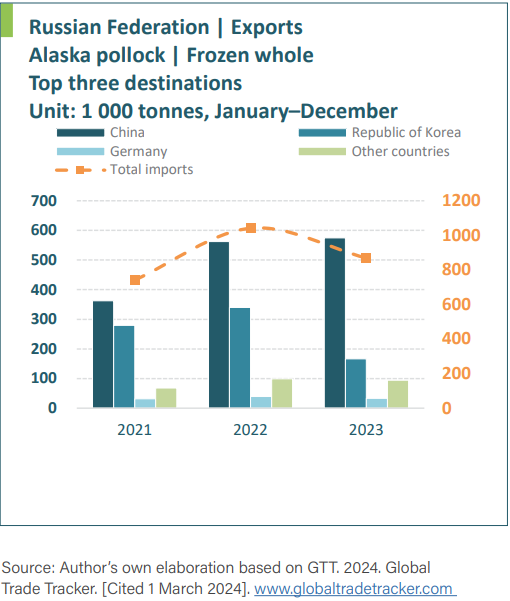

Russian exports of whole frozen Alaska pollock in 2023 were 868,406 tonnes, a fall of 16.6 percent over the previous year. The largest markets were China (66.2 percent of the total) and the Republic of Korea (19.2 percent of the total).

Surimi

While deals are being made for pollock surimi for the 2024 A season, Japanese buyers are showing reluctance to buy, possibly due to weaker consumer demand on the Japanese market.

Moreover, in Japan, the inventory for surimi is the largest in seven years, and this of course pushes prices down. According to Japan’s Ministry of Agriculture, Forestry and Fisheries, the total inventory of surimi in Japan at the end of 2023 amounted to 55,008 tonnes, six percent more than at the same time in 2022.

Chinese consumers have been used to buying surimi made from warm-water species. However, Russian surimi producers, who are increasing production from year to year, are now hoping to convert these consumers to adopt coldwater surimi based on Alaska pollock. Russian production of Alaska pollock surimi is estimated to reach about 80,000 tonnes in 2024, up from 54,000 tonnes in 2023. Chinese consumers have been used to buying surimi made from warm-water species. However, Russian surimi producers, who are increasing production from year to year, are now hoping to convert these consumers to adopt coldwater surimi based on Alaska pollock. Russian production of Alaska pollock surimi is estimated to reach about 80,000 tonnes in 2024, up from 54,000 tonnes in 2023.

In addition to expected higher demand for Alaska pollock surimi on the Chinese market, demand in the Russian Federation also seems to be on the way up.

Total consumption of surimi on the Russian market (including warm-water surimi imports) is estimated to be about 80 000 tonnes. Obviously, none of this currently comes from US production.

Outlook

The changes on the groundfish market that we have seen over the past year are most likely continuing through 2024 and beyond. Cod is becoming less available and continuously more expensive. There could be a shift in market orientation on the part of major producers like Norway, where the focus moves to high-end consumers, for example in Asia and North America.

Alaska pollock will be abundant in 2024, and prices may sink deeper.

Consequently, consumers may shift their preferences from cod to pollock, guided mainly by price considerations. In addition, there is growing competition from farmed freshwater whitefish.

The impact caused by the conflict in Ukraine is not likely to disappear in 2024.

Ever more serious restrictions on trade with the Russian Federation must be expected, particularly on the part of the United States. At the same time, other western nations are also likely to tighten their restrictions on Russian trade.

Source: Globefish/FAO

[email protected]

www.seafood.media

|

Print

Print