|

Photo: FAO/FIS

Globefish report on the global lobster market

WORLDWIDE WORLDWIDE

Friday, July 19, 2024, 06:00 (GMT + 9)

The following is an excerpt from a report published by Globefish (FAO):

Supply shortage and very high prices

Poor landings during the winter have led to tight supplies of North American lobsters this spring. Consequently, prices have risen very high, and are expected to stay at that level until the fishing gets underway again in mid-May. Market demand is strong both in Asia and the United States.

Supplies

A study by the Canadian Centre for Marine Applied Research (CMAR) may have some good news for the Nova Scotia lobster industry. According to their findings, warmer waters should not pose a high risk for lobsters over the next 30 years. CMAR has projected how water temperatures could heat up in the lobster fishing areas around Nova Scotia but concluded that the average surface and bottom ocean temperatures during the warmest periods until 2055 will remain within optimal threshold levels. In other words, average water temperatures would still be within the ranges that lobsters in different life stages can withstand.

However, global warming will still affect the fishery. Due to storms and bad weather, lobster fishers are losing about one-third of their fishing days at sea, and this is expected to increase further. One way to meet this challenge would be to improve vessel safety, emergency response, vessel design and fishing dates, according to CMAR.

Poor landings in Maine and Atlantic Canada during the past winter were blamed on unusually cold waters and bad weather, forcing the fishers to go further out from shore. The resultant lobster shortage in Canada affected the market and prices in late 2023 and in the first quarter of 2024. However, these problems are not expected to continue into the second and third quarters of 2024 as spring weather sets in and water temperatures rise.

About 40 Canadian lobster vessels are participating in the fisheries on the Atlantic coast, and the various lobster grounds are expected to open by midMay. The combined annual production is expected to be around 100,000 tonnes

The Maine lobster fishery – the largest in the United States – landed less lobsters in 2023 compared to 2022. According to estimates by the Maine Department of Marine Resources (DMR), lobster fishers landed 42,517 tonnes of lobster during 2023. This was five percent lower than in 2022 but prices were up as a consequence of tighter supplies, and the firsthand value increased from USD 392.5 million in 2022 to USD 464.4 million in 2023.

Photo: YouTube

One reason for the lower landings could be that fewer lobster fishers were active in 2023. Only 5,372 lobster licenses were issued for 2023, compared to 5,643 in 2022 and 5,763 in 2021.

Markets

December and January are usually good catch months, while February is often cold and the bad weather affects landings. Inventory levels are estimated to be just ten percent of capacity and this is exacerbated by the fact that there is little stock carried over from the previous spring season. In addition, wharf prices in Canadian Nova Scotia were up by 31 percent in early 2024, and they are expected to further increase. Fishers got as much as CAD 17.00 (USD 12.52) per pound, compared to CAD 13.00 (USD 9.57) in February 2023.Most observers do not expect things to change for the better until mid-May, causing first-hand prices to go as high as CAD 20.00 per pound (USD 14.73).

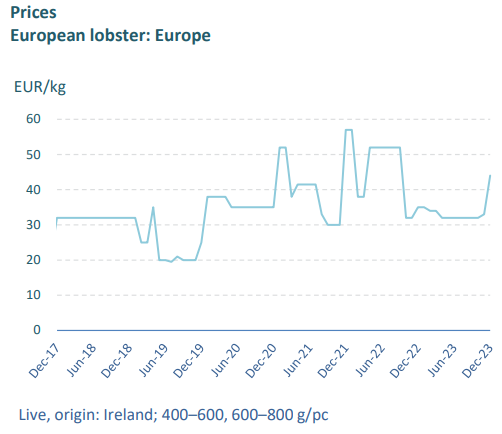

Source: Author’s own elaboration based on the European Price Report. 2024. GLOBEFISH. [Cited 1 March 2024]. www.globefish.org

For processors, such price levels are just too prohibitive; they need prices closer to CAD 10.00 per pound (USD 7.36). It is also feared that the high prices may scare consumers away from lobsters. Consequently, some lobster restaurants in the Republic of Korea are now reluctant to buy new stock, and may take North American lobster (Homarus americanus) off their menus.

International trade

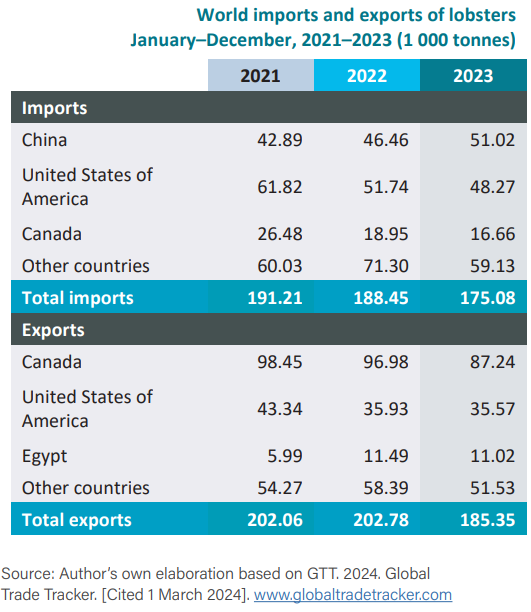

World trade in lobsters continued to decline in the fourth quarter of 2023, bringing the total exports for the year to 185,350 tonnes, down by 8.6 percent compared to 2022. Among the leading exporters, none registered an increase, while the top importer, China, saw an increase of 9.8 percent in lobster imports, at 51,020 tonnes. World trade in lobsters continued to decline in the fourth quarter of 2023, bringing the total exports for the year to 185,350 tonnes, down by 8.6 percent compared to 2022. Among the leading exporters, none registered an increase, while the top importer, China, saw an increase of 9.8 percent in lobster imports, at 51,020 tonnes.

In 2023, the lobster trade from North America to Asia was up by five percent in volume, back to pre-COVID levels. Exports to China, Hong Kong SAR and Viet Nam were good, but during 2018 and 2019, Chinese tariffs almost eliminated US exports to China.

Canada took over part of this trade and initiated direct cargo flights from Nova Scotia to China. Consequently, although total Canadian lobster exports fell by 11.7 percent to 77,554 tonnes, the only major market that registered growth was China, which absorbed 5.8 percent more in 2023 compared to 2022.

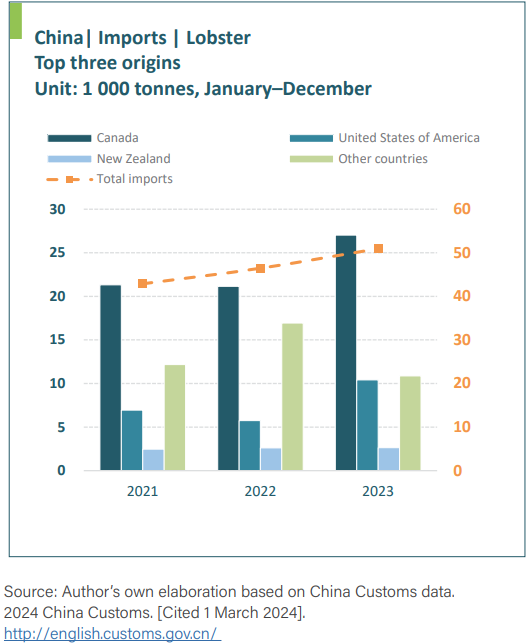

In fact, in 2023, Canada surpassed the United States as the biggest supplier of lobster to China. Also, for the first time ever, China became the largest market for live Canadian lobster with imports of 24,480 tonnes worth USD 390 million, up by six percent and 14 percent by volume and value compared to 2022. Imports of lobster from the second largest supplier, the United States, rose by a massive 81 percent to 10,416 tonnes, while imports from other suppliers declined. In 2023, China accounted for 45 percent of Canada’s total live exports of lobsters and other species, amounting to 53,998 tonnes.

The main reason for this development seems to be that Chinese consumers are eating more lobster. There is a growing middle class with good spending power in China, and lobster has always been high on the list of the most popular luxury seafoods.

Canadian lobster exports to the United States fell by 11.5 percent to 32,192 tonnes, of which live lobster amounted to 18,365 tonnes worth USD 621.5 million in 2023.

US exports fell marginally in 2023 to 34,978 tonnes, down by 1.2 percent. The largest market was, as usual, Canada, which accounted for 45.7 percent of the total. The second largest market, China, accounted for 11,621 tonnes or 33.2 percent of the total.

European imports fell by just over 20 percent in 2023 to 29,894 tonnes. The largest supplier was Canada, with 9,312 tonnes or 31.2 percent of the total.

Outlook

Supplies of North American lobsters (Homarus americanus) will continue to be rather tight for the next few months but are expected to improve by the end of May. Thus, prices will rise during the first quarter of 2024, and they will most probably go even higher by the end of April.

Market demand is good and improving after the COVID-19 pandemic; and sales in China, Hong Kong SAR and Viet Nam are on the way up. The US market is also recovering, but US domestic supplies are not up to previous levels. In Canada, supplies are expected to improve considerably by May.

Prices for all lobster products are anticipated to remain high through April, and processors may face problems finding raw material at low enough prices to make their operations worthwhile

Source: FAO-Globefish

[email protected]

www.seafood.media

|

Print

Print