|

Analysis on the global fish economy in-depth

FAO: GLOBEFISH Highlights Second Issue 2024

WORLDWIDE WORLDWIDE

Tuesday, July 16, 2024, 06:50 (GMT + 9)

Consumer sentiment remains poor despite improved economic prospects in both the United States and the European Union.

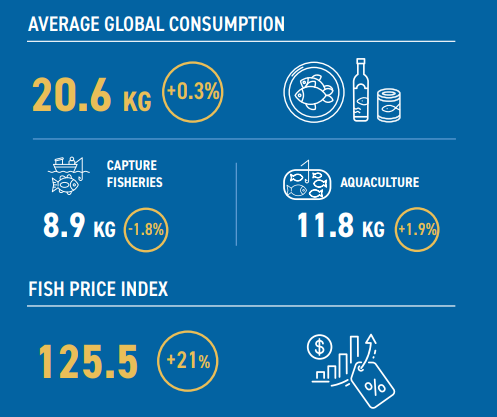

The years 2021 to 2023 saw the highest inflation rates in decades, and although economic growth and employment have exceeded expectations, consumer confidence remains affected by concerns about diminished purchasing power. This cautious sentiment has particularly impacted the demand for fisheries products, with many choosing other, often cheaper, protein sources. The FAO Fish Price Index (FPI) remained stable at 119 points in February 2024, indicating a balance between elevated prices for capture fisheries products and lower average prices for aquaculture products. Notably, farmed shrimp prices have dropped considerably, marking a 31 percent decrease over the past decade

Global fish economy

Growing uncertainty for global trade

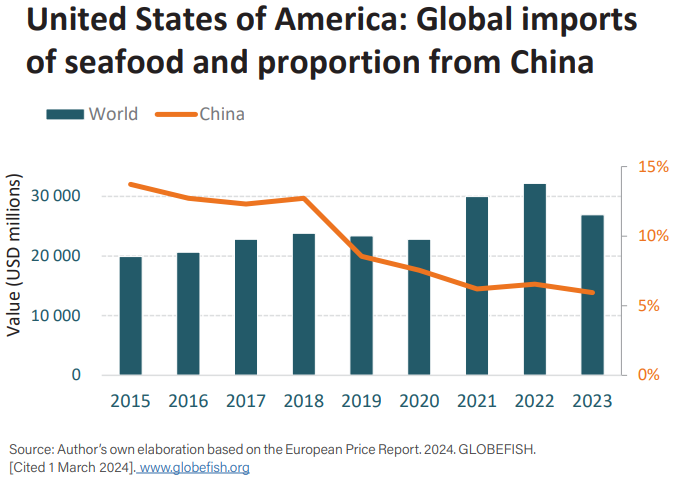

On 29 March 2024, the government of the United States of America (the United States) enacted additional trade-restrictive measures on goods from China, placing a slew of regulations and tariffs on various products. While these new restrictions are currently limited to aluminum, batteries, electric vehicles, medical equipment, solar panels and steel, there is widespread anxiety that the consequences will be far more wide-reaching and undermine the current global trade system.

This action certainly marks the latest and one of the most significant escalations in the ongoing tit-for-tat contest that has come to define the trade conflict between the United States and China. Starting in 2018, this has seen tariffs of up to 25 percent on fish and fisheries products in bilateral trade of both the United States of America and China. The disruption to global seafood trade has been marked and continues to be keenly felt. Tariffs and retaliatory measures imposed by both countries have led to increased costs and reduced market access for seafood exporters and importers.

US seafood producers, particularly those dealing in high-value products such as lobster and salmon, have faced steep declines in Chinese demand due to hefty tariffs, forcing them to seek alternative markets and absorb financial losses. Conversely, China’s processing industry, which imports large volumes of US-caught fish for processing and re-export, has experienced supply chain disruptions. This geopolitical tension has prompted a realignment in global trade routes, with both countries looking to diversify their trading partners and reduce dependency on each other.

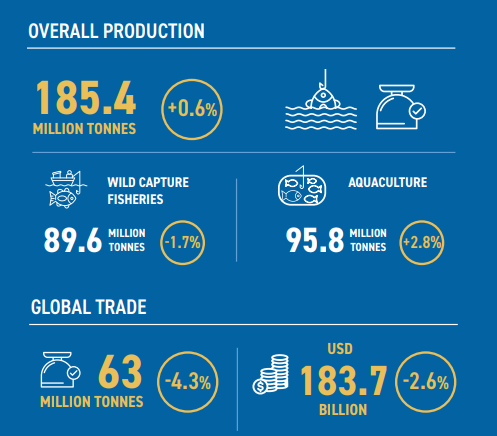

Forecasts indicate global fish production will surpass 190 million tonnes in 2024, with aquaculture contributing over 100 million tonnes for the first time and capture fisheries remaining under 90 million tonnes. Capture fisheries are projected to see a modest increase of 0.2 percent over 2023 levels, benefiting from easing El Niño conditions whichhave alleviated pressures on key fish stocks. Improved quotas for major species such as the Peruvian anchoveta, historically the largest fishery in the world, and Alaska pollock, the second largest by volume, are expected to add considerably to their supply. However, reduced quotas for other major fisheries, particularly cod and tuna, mean that global catches will remain largely flat. Meanwhile, aquaculture production is forecasted to grow by 3.3 percent to 100.8 million tonnes, driven by higher outputs of farmed shrimp and modest increases in oyster, carp and tilapia.

Consumer sentiment remains poor despite improved economic prospects in both the United States and the European Union.

The years 2021 to 2023 saw the highest inflation rates in decades, and although economic growth and employment have exceeded expectations, consumer confidence remains affected by concerns for diminished purchasing power. This cautious sentiment has particularly impacted the demand for fisheries products, with many choosing other, often cheaper, protein sources. The FAO Fish Price Index (FPI) remained stable at 119 points in February 2024, indicating a balance between elevated prices for capture fisheries products and lower average prices for aquaculture products. Notably, farmed shrimp prices have dropped considerably, marking a 31 percent decrease over the past decade.

The disparity between capture fisheries and aquaculture prices has led to varying impacts on global trade. Lower prices for aquaculture products have resulted in a predicted 1 percent decline in global trade values for 2024, amounting to USD 183.3 billion, with trade volumes expected to see a slight 0.3 percent decrease compared to 2023. The aquaculture sector faces profitability challenges due to low product prices and high production costs, exacerbated by the continued high prices of fishmeal and fish oil, which are essential inputs.

Read more analysis on the global fish economy an in-depth analysis for 13 species and commodity groups in the full publication.

Download publication

[email protected]

www.seafood.media

|

Print

Print