|

Photo: Rabobank/FIS

Rabobank Warns of 2028 Fishmeal Shortage Amid Slowing Protein Growth

WORLDWIDE WORLDWIDE

Monday, December 15, 2025, 00:20 (GMT + 9)

Seafood and Poultry to Lead 2026 Protein Growth as Industry Faces Supply Chain Pressures

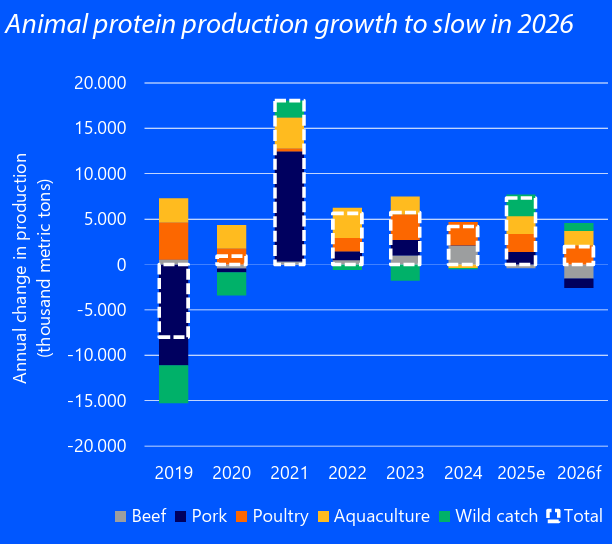

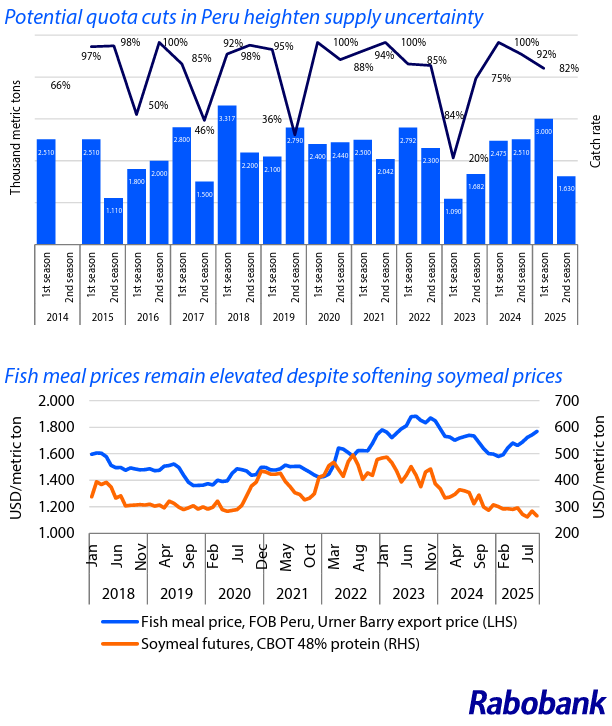

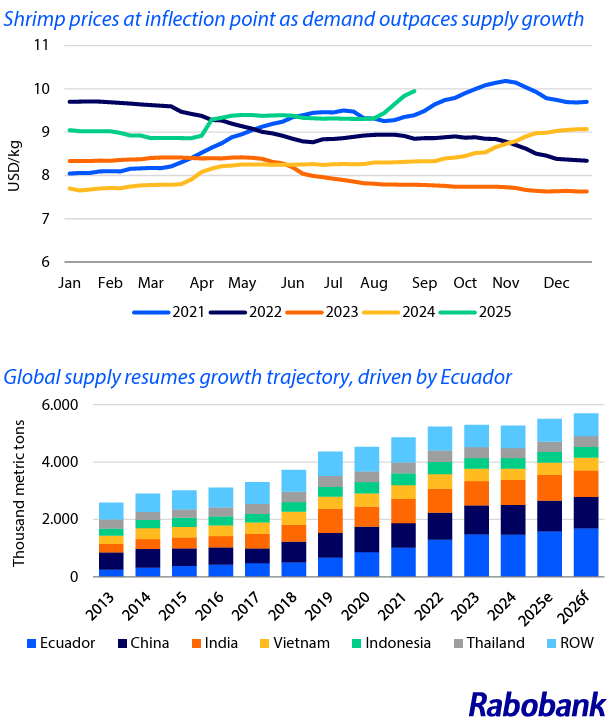

Rabobank analysts are forecasting a potential severe global fishmeal shortage beginning in 2028 unless the aquaculture industry implements timely and comprehensive countermeasures. The warning comes as the broader global animal protein production growth is expected to continue its slowdown into 2026.

Rabobank's analysis indicates that feed manufacturers are approaching the mandatory minimum usage levels for marine raw materials. Concurrently, global catch volumes have reached their ceiling, as most fisheries are operating within quotas. The bank projects that demand could exceed supply when the El Niño weather pattern is anticipated to return in 2028 if the consumption of fishmeal and fish oil is not further reduced.

To mitigate this impending supply pressure, Rabobank is urging the industry to adopt a multifaceted strategy rather than relying solely on market forces. Key suggestions include adjusting feed formulations to decrease the proportion of marine ingredients, increasing the use of fish by-products for meal and oil production, and expanding the utilization of new ingredients. These alternative supplements, such as algal oil, insect meal, and single-cell protein, are seen as potential sources to fulfill protein and omega-3 requirements in aquaculture, though cost and scalability remain significant challenges. Crucially, the bank emphasized the need for a shift from short-term transactional relationships to strategic partnerships to ensure sustainable, long-term raw material supply, attract investment, and expand production capacity of these alternatives.

Looking at the immediate future, Rabobank's Global animal protein outlook 2026 predicts that seafood will remain the primary driver of production growth, closely followed by poultry. Conversely, the output of beef and pork is projected to decline, which would mark the first reduction in global terrestrial species output in six years.

.png)

The 2026 outlook highlights several ongoing challenges that will weigh on margins. While feed costs are expected to remain steady, lower protein supplies, increasing volatility, rising trade costs, and persistent disease pressure will impact profitability. Processors may face difficulties with capacity utilization and trade disruptions from tariffs and other protectionist measures. With global GDP growth projected to slow, consumers will remain price-sensitive, leading to shifts in consumption patterns.

Furthermore, disease outbreaks, including recurring threats like African swine fever and avian influenza, along with emerging diseases such as New World screwworm, Bluetongue, foot-and-mouth disease, and lumpy skin disease, are disrupting trade, pressuring margins, and hindering productivity. This is driving greater adoption of biosecurity measures. The report also stresses that addressing sustainability-related risks linked to climate and nature is now essential, driven in part by regulatory momentum like the rise in climate-related financial disclosure legislation.

In this volatile environment, Rabobank advises animal protein companies to pursue diversification and consolidation while adapting portfolios to shifting consumer preferences. Technology, particularly the strategic integration of artificial intelligence (AI) into existing workflows, is also viewed as a pivotal tool for managing operational risks and advancing sustainability goals, despite traditionally weak investment in the sector.

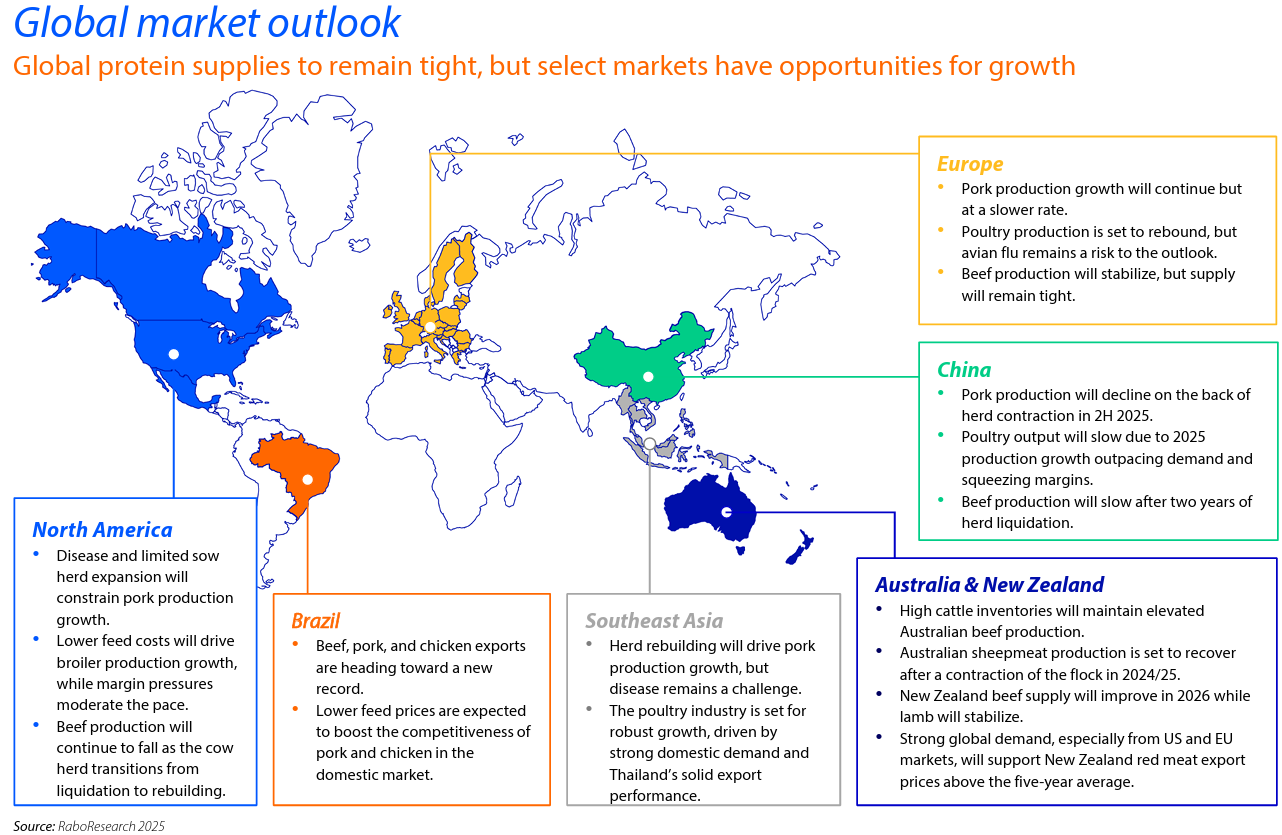

Key animal protein markets in 2026

North America

- Disease and limited sow herd expansion will constrain pork production growth.

- Lower feed costs will drive broiler production growth, while margin pressures moderate the pace.

- Beef production will continue to fall as the cow herd transitions from liquidation to rebuilding.

Brazil

- Beef, pork, and chicken exports are heading toward a new record.

- Lower feed prices are expected to boost the competitiveness of pork and chicken in the domestic market.

Southeast Asia

- Herd rebuilding will drive pork production growth, but disease remains a challenge.

- The poultry industry is set to record strong growth, supported by export demand as domestic markets rebalance.

Click on the image to enlarge it

Australia & New Zealand

- High cattle inventories will maintain elevated Australian beef production.

- Australian sheepmeat production is set to recover after a contraction of the flock in 2024/25.

- New Zealand beef supply will improve in 2026 while lamb will stabilize.

- Strong global demand will support New Zealand red meat export prices above the five-year average.

China

- Pork production will decline on the back of herd contraction in 2H 2025.

- Poultry output will slow due to 2025 production growth outpacing demand and squeezing margins.

- Beef production will slow after two years of herd liquidation.

Europe

- Pork production growth will continue but at a slower rate.

- Poultry production is set to rebound, but avian flu remains a risk to the outlook.

- Beef production will stabilize, but supply will remain tight.

Read the full report

Global Animal Protein Outlook 2026

[email protected]

www.seafood.media

|

|

.png)

Print

Print