|

Photo: Mowi ASA

Mowi Achieves Record Q3 Volumes Despite Low Salmon Prices

NORWAY

NORWAY

Thursday, November 06, 2025, 00:10 (GMT + 9)

Integrated Strategy Drives Strong Performance as Company Raises 2025 Guidance

Mowi has reported record-high volumes in the third quarter (Q3), delivering a solid result despite a challenging period marked by low salmon prices due to high supply growth.

.png) The company posted revenues of EUR 1.39 billion and an operational EBIT (Earnings Before Interest and Taxes) of EUR 112 million for the quarter. The company posted revenues of EUR 1.39 billion and an operational EBIT (Earnings Before Interest and Taxes) of EUR 112 million for the quarter.

Mowi CEO Ivan Vindheim highlighted the operational success and growth, stating, “Despite the quarter’s challenging prices it is pleasing to see that we continue to deliver well on both operations and growth. We have never produced more salmon than we did this quarter and we have never had more fish in the sea at this time of year. All of which positions us well for further growth.”

-

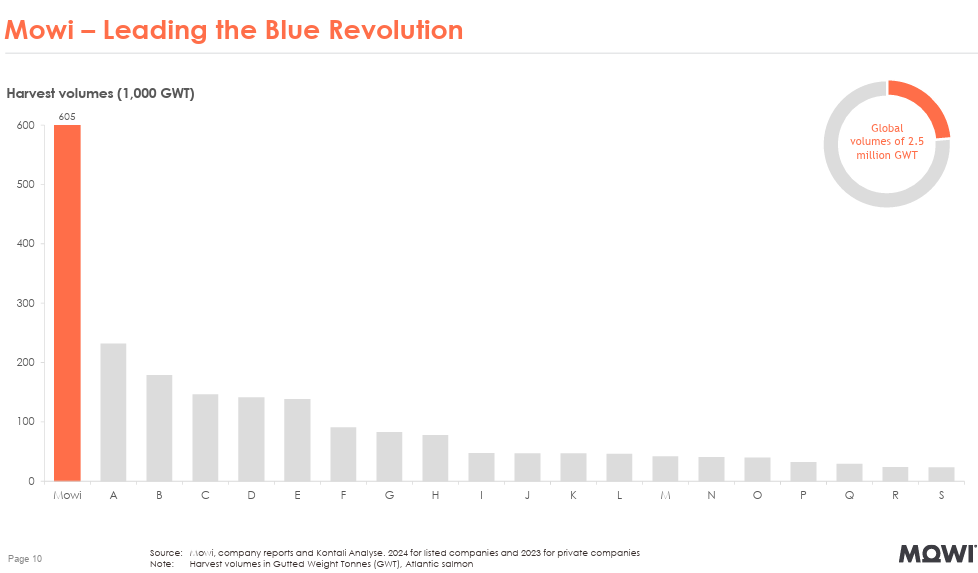

Record Harvest: Mowi harvested a record 166,000 tonnes in the third quarter.

-

Revised Guidance: The company is raising its volume guidance for 2025 once again, from 545,000 tonnes to 554,000 tonnes. This increase is mainly a result of consolidating Nova Sea from the fourth quarter, corresponding to a growth of 10.5% from 2024.

-

Future Growth: Mowi expects to harvest 605,000 tonnes in 2026, up 9.2% from the current year, with 380,000 tonnes of that total to be harvested in Norway.

Click on the image to enlarge it

Cost Reduction and Segment Success

Mowi has successfully evolved from a 400,000-tonne farmer to a 600,000-tonne farmer in just a few years, simultaneously developing into one of the most profitable aquaculture companies through a strong focus on costs.

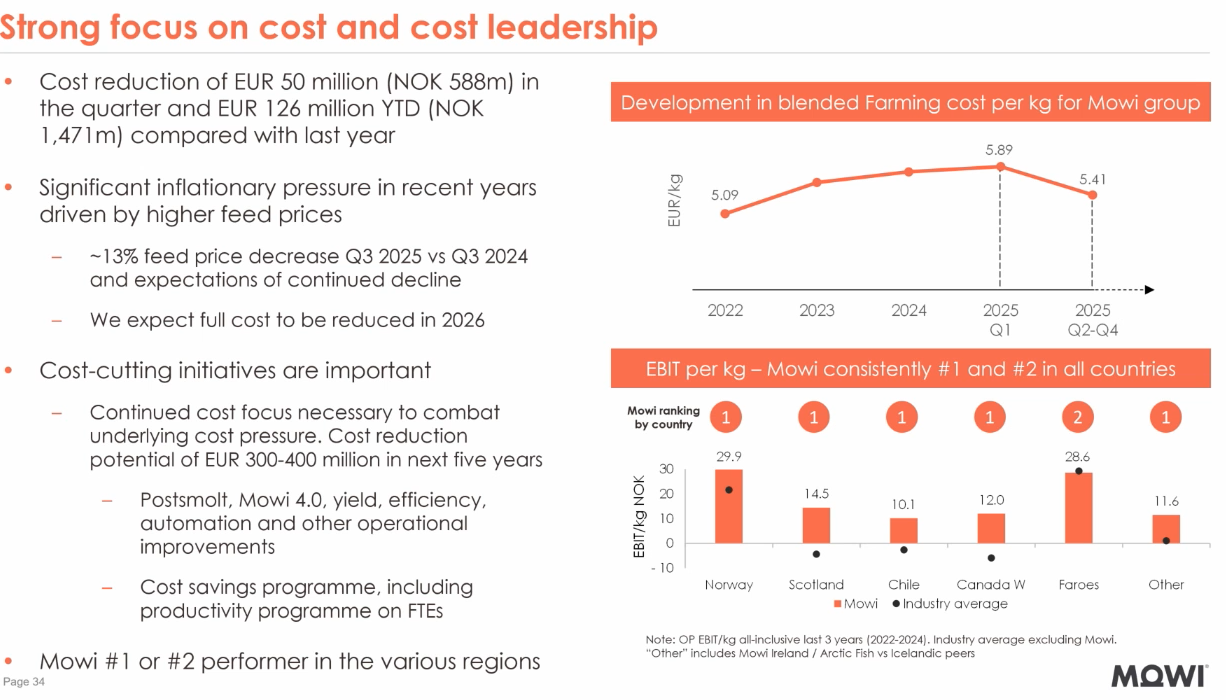

Vindheim noted significant cost reductions, saying, “It is positive to see that we have reduced our farming costs by a full EUR 50 million in the third quarter this year compared with the same quarter last year, and by EUR 126 million in the year to date. Furthermore, our standing biomass cost continues to develop positively on lower feed prices and other cost measures, which bodes well for next year’s realised production costs.”

Click on the image to enlarge it

Both the processing and feed divisions delivered robust results:

-

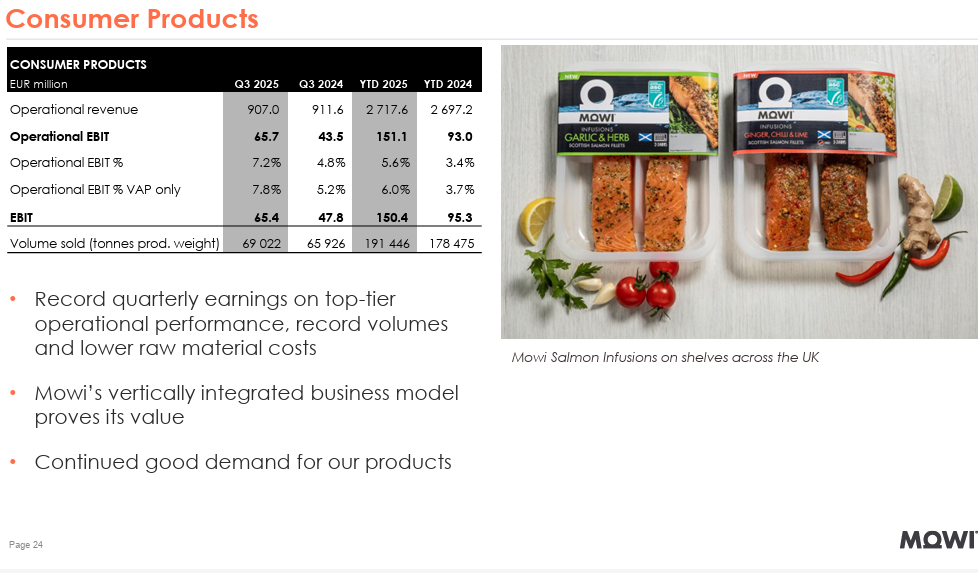

Mowi Consumer Products (the group’s processing business) delivered its best quarter ever with very good operations, record-high volumes, and lower raw material prices. Vindheim emphasized the benefit of integration, allowing the downstream segment to "buy cheaper raw materials and exploit market opportunities in periods of falling salmon prices, as in 2025."

-

Mowi Feed delivered a strong quarter with record-high earnings and its second-highest sales volumes ever.

Click on the image to enlarge it

Market Outlook and Dividend

2025 was marked by abnormally high supply growth, following several years of challenging biology for the industry. However, supply growth is now normalizing and is expected to be around 1% next year. This, combined with good market prospects, means Mowi anticipates a tighter market balance going forward.

The board of Mowi has decided to pay a quarterly dividend of NOK 1.50 per share.

Full report here

[email protected]

www.seafood.media

|

.png)

.png)

.png)

Print

Print